7 april 2023 - De Nederlandse regering wijzigingen gepubliceerd in de toepassing van de vrijstellingsmethode voor bestuurdersvergoeding van statutaire bestuurders en commissarissen in het buitenland.

In het algemeen wordt het inkomen van statutaire bestuurders en commissarissen (verder: bestuurders), inwoners van Nederland, belast in het land waar de vennootschap is gevestigd. Om dubbele belasting te voorkomen wordt in de meeste belastingverdragen de verrekeningsmethode toegepast. Dit betekent dat de in het buitenland betaalde belasting in mindering wordt gebracht op de in Nederland verschuldigde inkomstenbelasting over het wereldinkomen (inclusief de bestuurdersvergoeding). Dit kan leiden tot een extra bedrag aan Nederlandse belasting indien de in het buitenland betaalde belasting lager is dan de in Nederland verschuldigde belasting.

Op grond van een in 2008 gepubliceerd besluit van de staatssecretaris van Financiën konden bestuurders de vrijstellingsmethode toepassen met betrekking tot hun bestuurdersvergoeding in hun Nederlandse aangifte inkomstenbelasting, onder de volgende voorwaarden:

De vergoeding van bestuurders is feitelijk in het buitenland belastbaar;

en in het buitenland is er geen gunstiger regime voor dergelijk inkomen dan voor een standaard arbeidsinkomen.

De vrijstellingsmethode bestaat uit een vermindering van de verschuldigde Nederlandse inkomstenbelasting. Kort samengevat wordt de vermindering als volgt berekend:

Buitenlands inkomen / wereldinkomen * verschuldigde inkomstenbelasting over wereldinkomen

De uitkomst van deze berekening is de vermindering van de in Nederland verschuldigde belasting over het wereldinkomen. Indien de berekende vermindering hoger is dan het bedrag aan in het buitenland betaalde belasting, wat meestal het geval is, is er sprake van een voordeel.

Op 13 juli 2022 heeft de staatssecretaris aangekondigd dat bovenstaande mogelijkheid per januari 2023 wordt afgeschaft. Hierdoor kunnen bestuurders geen gebruik meer maken van de vrijstellingsmethode, maar geldt vanaf 1 januari 2023 de verrekeningsmethode. Als gevolg van deze wijziging kunnen in Nederland wonende bestuurders die werkzaamheden verrichten als bestuurder van een buitenlandse vennootschap een lagere netto vergoeding ontvangen voor hun bestuurderswerkzaamheden.

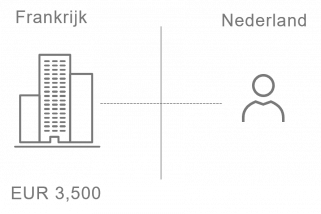

Ter verduidelijking van de fiscale gevolgen vindt u hieronder een voorbeeld.

Voorbeeld

Een Nederlandse inwoner is bestuurder van bedrijf X, die in Frankrijk is gevestigd. Dit bestuurslid ontvangt een jaarlijkse vergoeding van € 25.000. Deze beloning wordt in Frankrijk effectief belast tegen een tarief van 14%, vergelijkbaar met het Franse loonbelastingtarief. Hiermee wordt voldaan aan de Nederlandse voorwaarden voor het verlenen van belastingvermindering met de vrijstellingsmethode. Dit betekent dat de Nederlandse bestuurder slechts een bedrag van € 3.500 (€ 25.000 x 14%) aan Franse inkomstenbelasting betaalt en geen inkomstenbelasting in Nederland.

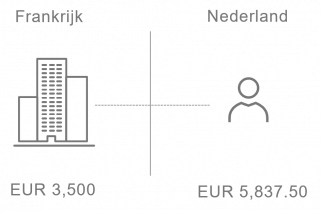

De afschaffing van het Nederlandse belastingbeleid, aangekondigd door de staatssecretaris op 13 juli 2022, zal per 1 januari 2023 tot een andere uitkomst leiden. De door Nederland verleende belastingvermindering zal daarom gebaseerd zijn op de creditmethode. Deze belastingaftrek bestaat uit een aftrek van de verschuldigde Franse belastingen op het totale bedrag van de Nederlandse inkomstenbelasting die over de vergoeding verschuldigd is. Op die manier wordt de Nederlandse bestuurder van de Franse vennootschap op dezelfde manier belast als een Nederlandse bestuurder van een Nederlandse vennootschap. Het totale bedrag aan Nederlandse inkomstenbelasting dat over de beloning verschuldigd is, bedraagt € 9.337,50 (€ 25.000 x 37,35%). Dit bedrag wordt verminderd met de in Frankrijk betaalde inkomstenbelasting (€ 3.500 (€ 25.000 x 14%)), wat resulteert in een bedrag van € 5.837,50 aan Nederlandse inkomstenbelasting.

Dit voorbeeld laat zien dat op basis van het huidige Nederlandse belastingbeleid, het Nederlandse bestuurslid van een Franse vennootschap in totaal € 3.500 aan inkomstenbelasting zal betalen. Per 1 januari 2023 moet het Nederlandse bestuurslid zowel Franse als Nederlandse inkomstenbelasting betalen, wat resulteert in een totaalbedrag van € 9.337,50.

Meer weten?

Wilt u graag meer weten over deze aangekondigde wijzigingen? Neem dan contact op met Alexander Rasink per e-mail of per telefoon +31 (0)88 277 1615 of met Madelon Warning per e-mail of per telefoon +31 (0)88 277 2426. Zij helpen u graag.

24 maart 2022 - De Advocaat-Generaal (A-G) van het Hof van Justitie (HvJ) EU heeft het volgende in een tweetal zaken geconcludeerd: wanneer buitenlandse uitzendkrachten tussen twee arbeidscontracten in geen werk hebben in Nederland, dan is de sociale zekerheidswetgeving van de woonstaat van toepassing. Deze conclusie kan van belang zijn voor Nederlandse uitzendbureaus die werknemers in dienst hebben...

Is uw onderneming internationaal actief en maakt u gebruik van werknemers uit het buitenland? Dan moet u de fiscale en sociale-zekerheidsrechtelijke aspecten van uw personeel goed geregeld hebben. De specialisten van Mazars ondersteunen u bij alle aspecten van grensoverschrijdende arbeid. Zo kunnen uw expats zorgeloos van start met hun internationale opdracht.

Verricht uw bedrijf activiteiten in het buitenland? Dan krijgt u te maken met complexe internationale wet- en regelgeving. Weet u aan welke fiscale regels u moet voldoen? De specialisten van Mazars helpen u hiermee. Zij maken de fiscale gevolgen van uw internationale activiteiten inzichtelijk, zodat u de kansen voor uw onderneming optimaal kunt benutten.

De inkomstenbelasting is een belasting die wordt geheven van natuurlijke personen over inkomen uit arbeid, zoals winst uit onderneming, maar ook over inkomen uit de eigen woning, pensioen- en lijfrente-uitkeringen, inkomen uit een aanmerkelijk belang en inkomen uit sparen en beleggen.

Sommige zijn noodzakelijk, andere helpen ons bij het analyseren van het gebruik van de website, dienen advertenties of zorgen voor een gepersonaliseerd websitebezoek.

In onze privacy policy vindt u meer informatie over de cookies die wij gebruiken.